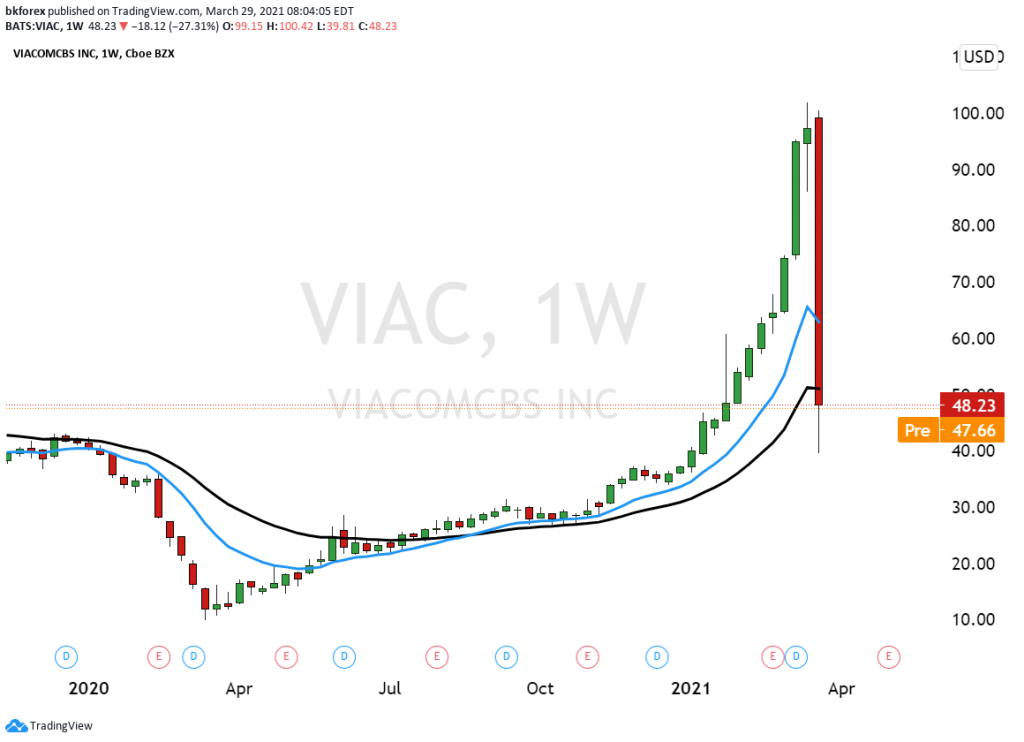

- Viacom -YOLO trade gone wrong

- Wallstreet bets? No

- Shadow world of equity swaps

- Could it destabilize the whole market?

Viacom stock (VIAC) the hodge-podge of old media assets of CBS and Viacom which includes a TV network, a smattering of cable channels and the Paramount movie studio was always suspect as a YOLO stock candidate. For most of last year it traded in a sleepy $20-$25 range but suddenly this year exploded to just above $101 before flaming out in one the most memorable crashes in recent history as it tumbled nearly 70% in a matter of days.

Viacom -YOLO trade gone wrong

Many analysts were puzzled why an old media company albeit with some mildly interesting assets but nevertheless low growth prospects would suddenly attract such a fervent following. The company was trying to repurpose itself as a streaming play, but as the fourth major entrant into the space it was hardly going to make a dent in consumer’s consciousness even though it offered NFL football and NCAA basketball. Live sports were certainly a pull, but in the grander scheme of things the sports fan demographic was just not enough to move the needle in making serious in-roads in market share in the new streaming world.

Wallstreetbets Again?

The stock found some love on r/wallstreetbets website where some of the retail speculators poured into the company’s option chain quickly snatching millions of profits in a matter of weeks. Still VIAC was a large capitalization stock and its ascent lacked the type of coordinated gang based behavior we’ve seen in stock such as GME or AMC

The Shadow World of Equity Swaps

It turns out the culprit behind the move was an off exchange transaction called an equity swap. An equity swap is a custom contract between two parties to exchange the difference in the value of a particular stock from the start of the contract until such time that the contract ends. For example if an investor wants to express a positive view on AAPL, the investor could enter into an equity swap trade with a bank at the current price of $121. If AAPL rises to $150 and the investor decides to close out the contract the bank would pay out $29. If however AAPL traded down to $100 then the investor would need to pay the bank $21.

An equity swap is simply a way for investors to bet on the underlying value of the security without actually owning the stock. If that sounds like a CFD ( a Contract for Difference) – it is. CFDs are an extremely popular retail product across the world but they are illegal in the United States. As derivative products CFDs offer several advantages – instant ability to go long or short the underlying security and most importantly, leverage.

Since outside of the US CFDs are mainly a retail product, the positions are small and even the use of leverage simply acts as a way of separating customers from their money rather than having any direct impact on the market for the underlying security itself.

In the US, equity swaps are an institutional product and therein lies the answer to the Viacom saga. It turns out that an offshore hedge fund called Archegos run by a former superstar manager manager Bill Hwang managed to amass a gargantuan position in Viacom stock without any formal disclosure through the use of equity swaps. As analyst Andrew Park noted, “Outside of the prime brokers providing leverage, few others knew Archegos held equivalent of >10% of the shares (of VIAC) due to the ongoing loopholes in Form 13-F reporting for derivatives positions”.

Could it destabilize the whole market?

Leverage is a two edged sword of course and as we already noted when it is applied to the retail order flow the spillovers are manageable. However, Mr. Hwang positions were so large and so concentrated that they managed to impact the whole equity market. On Friday the massive sell orders by Goldman Sachs and others looking to liquidate Archegos’ losing trades spooked the whole market taking the indices down in the afternoon. In the overnight action the same dynamic appears to be taking place as Goldman continues to liquidate Mr. Hwang’s positions.

Although the immediate impact of the Viacom blow up has been contained the whole sordid affair raises a slew of questions for regulators. How could an offshore fund run by a manager who has been fined by $44 Million by the SEC and effectively banned from doing business in the US establish such a large derivative position in the VIAC stock without any public disclosure? What happens if there are many such shadow transactions on the books that may need to be liquidated all at once? Could it create a cascade-like effect reminiscent of the 1987 “portfolio-insurance” fiasco? Should the CFTC – which has regulatory authority over equity swaps – step in, do an immediate audit of major positions and force all and any disclosures so that officials are not caught by surprise next time?

It will be interesting to see if the regulators take a proactive stance in this matter or simply let the issue fester until the next time. Meanwhile, VIAC shareholders will need to come to terms with the idea that someone who did not even own a share of their company managed to destroy 70% of the value of their assets in less than 48 hours.