- #USD Sells Off as Jobless Claims Spike

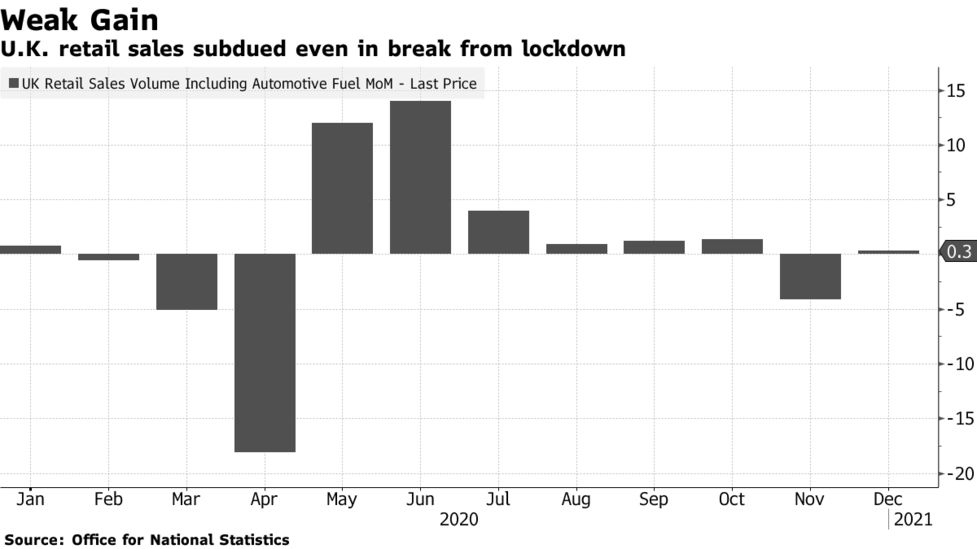

- #GBP Soars as Traders Eye 1.40, Retail Sales & PMI on Friday

- #EURGBP Falls to Lowest Level Since March 2020

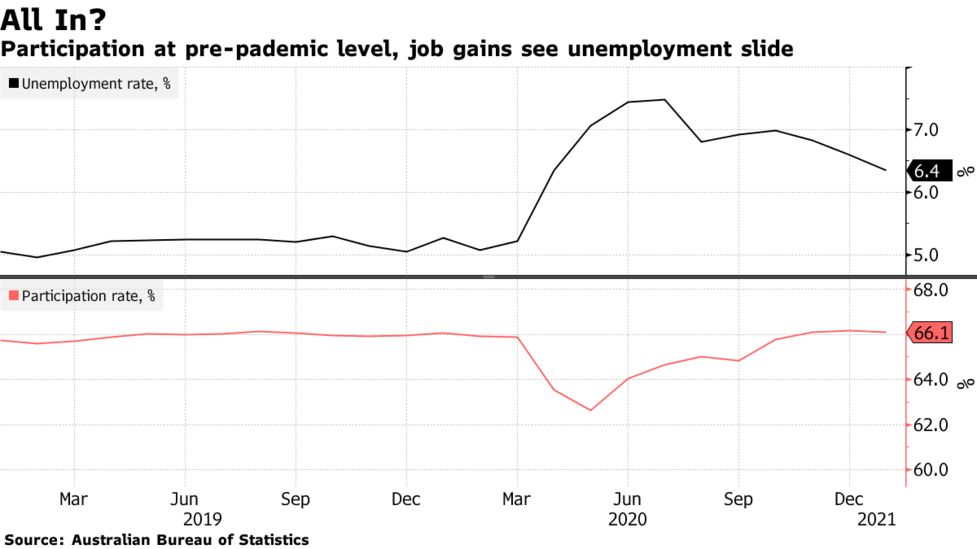

- #AUD Supported by Stronger Labor Data

- #EUR Rises Ahead of PMIs

- #CAD Unfazed by Lower Oil and Prospect of Weaker Spending

The post retail sales rally in the U.S. dollar did not last as the greenback resumed its slide against all major currencies on Thursday. This decline was somewhat surprising given the sell-off in U.S. stocks and rise in 10 year Treasury yields which typically coincides with a stronger dollar. However, the pullback was supported by economic data. While the Philadelphia Fed manufacturing index beat expectations, activity slowed from the previous month. Jobless claims also jumped from 793K to 861K last week. Building permits rose 10% but this improvement was offset by a drop in housing starts. Ultimately none of these reports are high impact data for the dollar but they reinforced the lack of demand for the greenback. Sterling benefitted the most from U.S. dollar weakness with GBP/USD traders driving the pair towards 1.40. With no UK data to spark these gains, the move was purely technical.

Friday will be a busy one for forex traders with many market moving economic reports scheduled for release. However the focus will be on other currencies and not the dollar because the only US release, existing home sales typically does not inspire big moves so instead, the dollar will take its cue from stocks and yields.

Keep an eye on sterling because the question of whether GBP/USD breaks or fails at 1.40 will be determined by Friday’s UK retail sales and PMI reports. We know from the British retail consortium’s own measure that consumer spending was very weak at the start of the year as they reported the slowest rise since May. Economists are also looking for a significant decline. Ongoing restrictions should to weaker PMIs even as we look forward to a strong second half recovery. All of this suggests that the path of least resistance for GBP/USD in the near term should be lower.

Eurozone PMIs are also on the calendar. Like the U.K., ongoing restrictions should mean subdued economic activity. Last week Germany extended its lockdown until March 14th at the earliest. Although new virus cases have come down significantly, the government is concerned about how rapidly the U.K. variant is spreading. The longer restrictions remain in place the longer it will take for the economy to recover. According to the ECB minutes, Eurozone policymakers felt that ample monetary stimulus remained essential. We are still looking for EUR/USD to test 1.20.

The Australian dollar traded higher on the back of a stronger labor market report. Although the total number of jobs created last month was less than expected and fewer than the previous month, the details of the report revealed more strength than weakness. All of the jobs lost were part time with full time employment growing by 59K. The unemployment rate also dropped to 6.4% from 6.6%, a sign that the country’s labor market recovery is intensifying. Australian retail sales and PMIs are due for release this evening. With the country in the midst of a post-COVID recovery, all signs point to stronger data. The same is true for New Zealand, which should see producer prices rise alongside consumer prices. The only outlier is Canada. Retail sales should be weak given the drop in wholesale sales and deterioration in labor market conditions.

Given the abundance of non-U.S. data, the greatest opportunities may be in currency crosses on Friday.