- #Dollar Soars on Strong Non-Farm Payrolls

- US Companies Added 545K Jobs Last 2 Months

- #EURUSD Drops to 3 Month Lows

- #USDJPY Falls to Weakest Level Since June 2020

- #CAD Resilient on Oil, Trade and IVEY

The U.S. dollar hit new highs on Friday after a strong U.S. jobs report. The greenback extended its gains against all of the major currencies with USD/JPY rising to its strongest level since June 2020 and EUR/USD falling to its weakest since November. Unlike prior days when there was less uniformity, all of the major currencies succumbed to the dollar’s rally. In fact, investors were bidding up the dollar before the number was released and when it came out, the gains accelerated as the labor market recovery reinforced Federal Reserve Chairman Powell’s optimism and the reflation trade. Stocks recovered from Thursday’s losses with further gains likely as the stimulus bill moves into final stages.

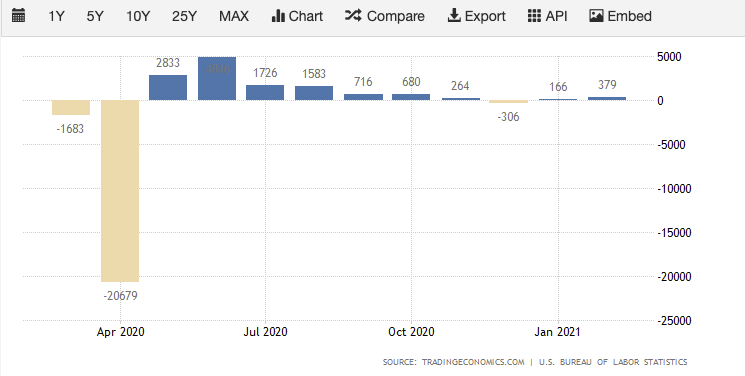

Thanks to reopening of restaurants and bars, the U.S. economy is gaining momentum and heading into spring on solid footing. U.S. companies added 379K last month, nearly two times expectations but what’s even more remarkable was the upward revision to January’s report. Initially only 49K jobs were reported but U.S. companies added 166K jobs, for a total of 545,000 new jobs over the last 2 months. With more than two thirds of February job growth attributed to the food service industry, it is clear how much impact less restrictions can have on the economy and what the U.S. can expect in the coming months as more Americans are vaccinated. The leisure and hospitality sectors will snap back and along with it, more job growth.

Non-Farm Payrolls

On March 14th, the extra $300 a week unemployment benefit will expire. The White House and Congress are committed to extending this aid and if they want to avoid a lapse, the stimulus package needs to be passed in the next 10 days. When an agreement is made, the announcement could provide another jolt to the stock market. But this time around, the dollar could fall as more fiscal spending reduces the greenback’s appeal.

Progress on the stimulus deal will be the most important driver of dollar flows in the coming week along with February’s consumer price report. CPI has not been a big mover for currencies over the past year but with rising inflation expectations driving the volatility in the bond market, investors may be particularly sensitive to inflation trends.

The European Central Bank and Bank of Canada monetary policy announcements will also be in focus. No changes are expected from either central bank but investors are keen to see If the central bank’s concerns about rising yields turns into stronger language or more action. Slow vaccine rollout, ongoing restrictions and new increases in coronavirus cases in Italy suggest that Eurozone will lag the U.S.’ recovery. EUR/USD was the worst performing major currency pair on Friday and the prospect of ECB dovishness could drive the pair down to the 200-day SMA at 1.18.

Next to the U.S. dollar, the Canadian dollar was the second best performer. Oil prices rose 3%, manufacturing activity expanded at a faster pace last month according to the IVEY PMI index which rose to 60 from 48.4 and the trade surplus rose more than expected. These good reports rivaled the NFP and allowed the Canadian dollar to hold onto its gains. While the Bank of Canada will be pleased to see these improvements, Canada is falling far behind the U.S. in Covid vaccinations which could be a big problem. Only 6% of their population is vaccinated compared to the U.S. where more than 16% Americans have received their first doses.