- DG is at 52 week highs but headwinds ahead

- Supply chain bottlenecks, wage pressures, consumer choice all problems for company

- A tactical way to play the correction

Whether inflation is transitory or durable continues to be the debate in the markets, but the very clear fact as shown in yesterday’s CPI data is that inflation is raging right now and while investors may dismiss its impact the reality is that it’s likely to take its toll on dollar retailers even sector leaders such as Dollar General.

There is no doubt that DG is an excellent company having grown sales at 10.6% rate over the past five years while earnings have compounded at a 17.9%. The company operates more that 17,000 stores in 47 states and is especially active in rural communities where its smaller footprint puts it at a distinct advantage over Walmart. It is also a very well run company producing free cash flow of 8.44% while sporting a dividend of 77 basis points and relatively modest P/E of 21. The company has just announced that it will move into healthcare products, increasing its assortment of health aids, medical, nutritional, dental, cough and cold, and feminine hygiene products across many of its stores.

The company is a well run machine and continues to be a very attractive long term investment. But over the next six month horizon the company is likely to face a host of external pressures not of its own making that could hamper growth and compress margins.

Supply side constraints

Although some of the worst supply side bottlenecks may be easing the fact remains that both sourcing of goods and especially the transportation of goods will continue to be a much higher expense going forward especially as crude prices remain above the $70/bbl mark. Because of the company’s “natural” cap of one dollar on most of its items DG will no doubt begin to feel greater margin pressure on goods sold. Although DG and many other dollar retailers have moved past the dollar mark on some of their items, consumers still associate that price as the anchoring point and may defect from the stores if they perceive a diminution of value.

Wage Pressures

Perhaps even more ominous than the supply chain issues is the increasingly tight labor markets for the company’s low wage jobs. There are some anecdotal reports that the company has to operate limited hours due to staffing constraints which not only affects the opening hours of the stores, but far more importantly the proper stocking and cleanliness of each box – a critical issue for sustained revenue gains

Consumer choice

Dollar General was a key beneficiary of the pandemic flows as its low cost offering was a perfect solution for cash strapped and bewildered consumers during the peak of COVID panic. However as the economy has recovered and consumer sentiment has improved markedly consumers may opt for more upscale choices putting additional stress on revenue growth.

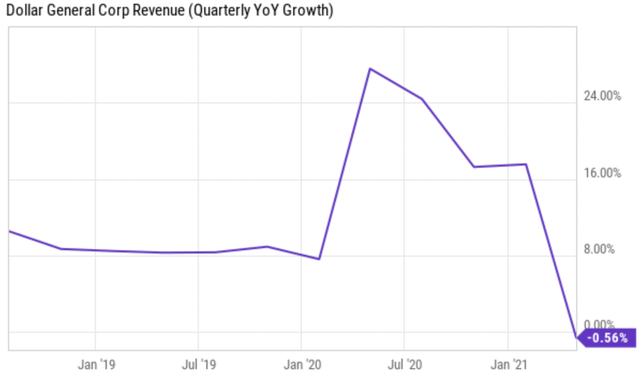

The chance of pace is already evident in the steep falloff in q/q growth.

Retreat from $220 Level?

Despite obstacles ahead DG stock has remained well bid trading near 52 week highs. However the stock shows multiple resistance at the $220 level going back a year. Given both the macro and the micro issues facing the stock DG may be a tactical short trade for the next six month going forward. The Jan 21 220/200 put spread is priced at $7 indicating that the market is assigning just a 35% probability that the stock will drift below the $200 level by year end. That may be too optimistic especially if the current environment of supply chain constraints and wage pressures continues to persist until the year end. While DG remains an excellent long term hold it may be due for a correction and Jan 21 220/200 put spread provides a limited risk approach to play that move.