- FAANGs blow away their numbers but market reaction muted – why?

- Triple plays only get half the benefit of the ten year average reaction

- Stock markets are upper range of valuation

- Time for stock substitute plays?

FAANGs blow away their numbers but market reaction muted – why?

Although the earnings season is only half over the key FAANG stocks all reported numbers with most blowing out their results well above consensus estimates. Yet the overall market is showing little follow through as the tech heavy Nasdaq trades lower this morning.

Yesterday Amazon was the last of the FAANGs to report numbers and the results did not disappoint with the company reporting earnings at 66% higher than expected with EPS coming in at $15.79 versus $9.64 forecast. With AMZN report coming on the heels of a very big beat by AAPL as well the data suggests that the high tech sector continues to benefit from secular growth even as the pandemic risk recedes.With global economy poised for a massive rebound in the summer the favorable business trends for all the FAANG stock with the exception of NFLX (see our prior report here) should continue.

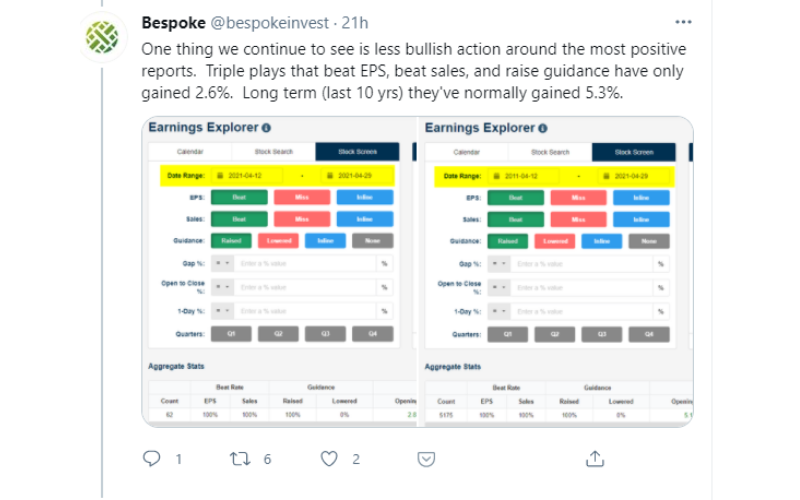

Triple plays only get half the benefit of the ten year average reaction

Yet the price action of the equity market is nowhere as ebullient as you would expect it to be.

As Bespoke Research noted, the Triple Plays – stocks that have beaten on top and bottom lines and have raised guidance only gained about one half as much as the ten year average. The muted reaction suggests that the valuation may have gotten ahead of itself and that stocks may chop around for the next quarter or two as investors assess the further upside of the return-to-normal trade.

Stock markets are at upper range of valuation

As Sven Herich points out, the US markets are now valued at 205% of the GDP and even if you take out the tech sector the valuation is stratospheric 173% to GDP.

Time for stock substitute plays?

None of this means that stocks are about to crash as the fundamental support behind the recovery remains sound. But it does suggest that investors should get more defensive despite the seemingly endless stream of good news. Those investors who have captured the upside move since last year’s March lows should consider a stock substitution strategy swapping out their equity positions for 6 month or longer dated options. With volatility relatively the excess premium costs are not onerous and if equities do drop 5% to 10% in a correction much of the short term damage to the portfolio could be avoided.

The strategy can be further enhanced by selling out of the money calls against the newly purchased options as the best case scenario for the next few months appears to be a slow grind higher given that much of the positive news is already baked in.