- Diversifying by market regime rather than asset class

- The “Moneyball of Money” approach

- Challenges for the DIY investor

In part one of our analysis of Chris Cole’s appearance on the Odd Lots podcast we took a look at the danger of the recency bias and the over reliance of investors on the 60/40 portfolio which has performed tremendously for more than a generation, but may now move into a massive multi-year path of underperformance due to a variety of factors including demographics, interest rates and de-globalization.

Diversifying by market regime rather than asset class

In this part we consider Mr. Cole alternative portfolio – an investment thesis that he calls the portfolio for 100 years – that is constructed quite differently from the traditional 60/40 stock/bond mix. Before we examine the specifics, it’s important to note that Mr. Cole central tenet is that investors should diversify across market regimes rather than asset classes. This is a very innovative idea as it addresses one of the key problems of diversification by asset – namely that in certain market regimes correlation moves to 1.0 providing no actual protection to the investor as many assets move in the same direction. This can certainly happen with a simple bonds and stock portfolio as there have been many periods in history when both stock and bonds fell at the same time, most recently during the pandemic crash of 2020. Indeed, one could make an argument that the massive gains of the 60/40 portfolio over the past 40 years are due simply to the incredibly long positive correlation cycle between bonds and stocks.

Mr. Cole highlights the dangers of projecting the past onto the future and suggests that investors need to be prepared for three distinct market regimes – deflationary crash, fiat devalue and growth and reflation. Typically during deflationary crashes cash, hard assets and long volatility strategies work best. Few investors realize that during the 1930’s realized volatility was 40% per year. It is as though the massively volatile year of 2008 repeated itself for a decade. Fiat devalue and growth such as we have now, favor equities and trend and momentum strategies. Finally, the reflation regime favors fiat alternatives, commodity-trend and equity assets.

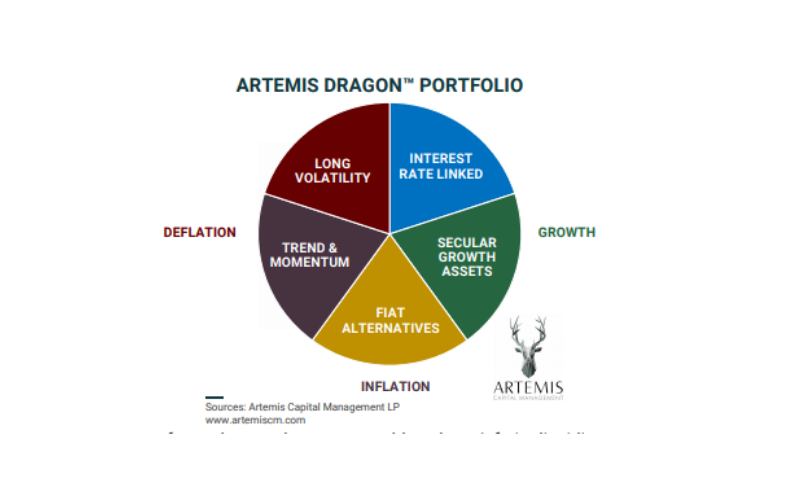

The “Moneyball of Money” approach

Mr. Cole’s portfolio construction consists of dividing the assets into approximately five equal buckets of allocation. These are interest rate linked assets (bonds, high dividend stocks etc.), secular growth assets (large cap and small cap stocks), fiat alternatives (precious metals and crypto), trend and momentum strategies (typically done by commodity pool operators) and long volatility. His argument is that investors should essentially create a “moneyball for money” approach where no one asset is superior but the sum of the parts is greater than the whole. Just as in baseball and soccer, teams have discovered that a combination of slightly better than average players can outperform an opponent with one big superstar. Mr. Cole’s contention is that a similar approach where no one asset will dominate performance in the long run is a much better approach to wealth building.

Challenges for the DIY investor

Recent history has certainly borne him out as 2020 which saw the presence of all three market regimes created a perfect laboratory test for Mr. Cole’s thesis which in turn generated a 50% return for his Dragon portfolio versus only a 15% gain for the 60/40 mix. There is however a big problem with Mr. Cole’s approach as he is the first to admit. It does not lend itself to a simple do-it-yourself construction like the traditional 60/40 portfolio which can be replicated with nothing more than a SPY and TLT ETF purchases. Investors could certainly add the fiat alternative component by buying the GLD ETF and adding bitcoin to the mix but its the trend momentum strategies and long volatility strategies that are hard to replicate because there are no good ETF and ETN products that can mimic these approaches. All of the ETF or ETN products that attempt to replicate these strategies rely on derivatives such as futures and options and inevitably lose net asset value to the cost of carry embedded in those products. Witness the disastrous performance of the OIL ETF when the futures market went into negative pricing. The slow drip of cost of carry fees in the derivatives markets almost ensures that any ETF or ETN in the volatility or trend space will lose money. That’s why Mr. Cole recommends professional money management of the portfolio as the only true way to achieve its results.

Still despite the practical obstacles to its construction, investors should still consider Mr. Cole’s ideas. At very least they could easily implement three out of five recommendations, but even on the matter of long volatility investors could consider a simple straddle strategy on the S&P 500 and on the idea of trend momentum they could try to implement a simple 200 day moving average strategy on the CRB index ETFs. Granted these far from perfect proxies but they would comply with the spirit of Mr. Cole’s thesis that robust performance depends on the preparation for every possible market regime.