- Goodbye WFH hello POW

- Netflix best growth days are behind it

- Company has massive need for capital

- NFLX vulnerable to rising rates

- DIS+ runaway success on pace for 250M subs

- Return to parks and cruises will boost revenues in 2021

- New DIS+ subs will purchases multiples of Disney merchandise

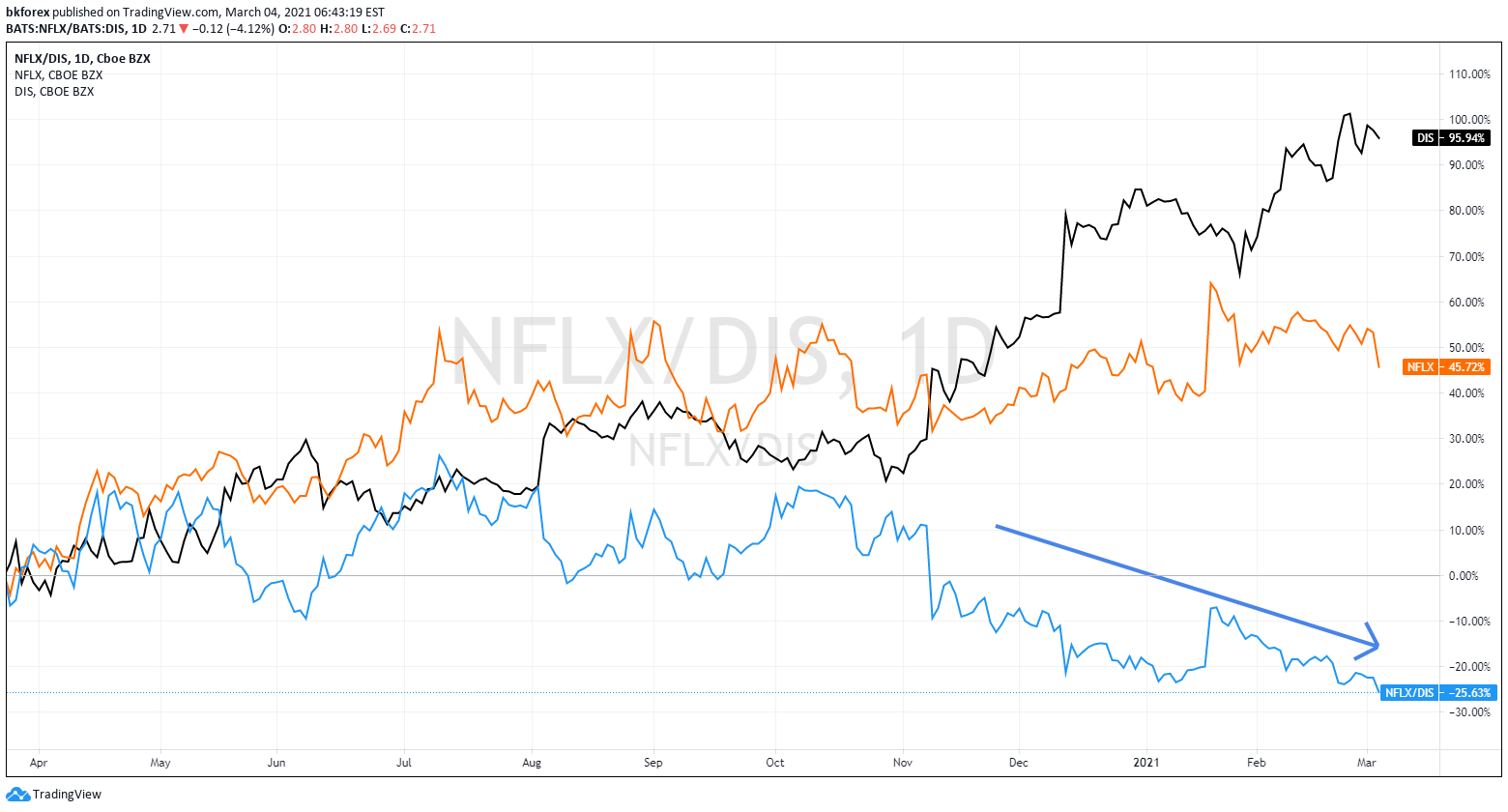

- Technicals confirm trade

A Clear Pair Trade in the Market

Say goodbye to WFH (work from home) and say hello to POW (play out in the world). As the rate of COVID vaccinations rises and the world moves closer to post pandemic return to normal one of the clearest pair trade opportunities in the market is short NFLX/ long DIS as one suffers and the other enjoys this upcoming shift in trend.

NFLX – best growth behind it

The COVID lockdown has been very good for NFLX which surprised the market with stronger than expected subscriber growth in its last quarterly call. But its best days of growth are behind it and the stock is likely to underperform as “Netflix and chill” loses its appeal with the budding warmth of spring in the air. The company faces not only a slowdown in subscriber growth but increasing competition from a panoply of new streaming services from small and large media companies alike which will make price increases – it’s primary strategy for revenue growth – prohibitively difficult to implement as some consumers may opt out of the service.

NFLX – Vulnerable to Rising Rates

Netflix has always had an insatiable need for capital in order to create content. It’s current debt load stands at 10B and its debt to equity ratio is nearly 1.5. The need for fresh content will not abate anytime soon, but in a rising interest rate environment the company is doubly vulnerable to a capital shock as its debt service costs are sure to rise if the 10Y yield eventually moves above the 2% barrier while at the same time its sky high valuation ( it trades at nearly 100 times trailing earnings ) will compress.

That could create a vicious cycle for the company as higher rates will make borrowing more expensive which in turn will impact earnings and stock price which will make the cost of borrowing even more expensive creating a negative feedback loop.

Disney – Primed for virtuous cycle

Disney on the other hand is about to enter a virtuous cycle as rapid vaccination of the population will unleash massive demand for its amusement parks and cruise business from consumers who are both stir crazy and flush with cash. Disney lost about 70% of its park revenue during the COVID shutdowns so just a return to its pre-pandemic levels will be a massive boost to its bottom line in 2021. Furthermore, the end of the lockdowns could not be happening at a more opportune time making the company’s travel and amusement properties available for the peak summer season.

DIS+ – massive merchandizing possibilities

But the re opening of the parks is only part of the story for Disney. During COVID the company released its streaming service DIS+ which has been a runaway success. The service was originally projected to garner 60M-90M subscribers by 2024. Now it is on pace to attract 250M subscribers by that date making DIS+ the only other truly global streaming platform in the market. Although DIS+ revenue per subscriber is considerably lower than Netflix’s and even declining from an average of $5 per month to closer to $4 as the company tries to establish a beachhead in lower income markets such as India, the longer term benefits of subscriber growth will more than offset by the recent decline in subscription rates. That’s because the company stands to make a multiple of subscription revenue from each new subscriber through merchandising.

Every new DIS+ subscriber becomes a new customer for Disney’s endless product offerings from toys to clothing to software. As DIS+ makes its way into nearly every middle class home on the globe its possibilities for increased revenue through merchandising are likely to skyrocket further enhancing the brand and the stock.

Technicals confirm trade thesis

With equities looking wobbly as stretched valuations and rising rates threaten the one way trade that has been in place for more than a year it’s a good time to consider a pairs trade to eliminate market risk and focus on absolute return. The long DIS short NFLX spread is not only a sound fundamental trade but is looking good on the charts as well. The spread has started to widen indicating that traders are warming to the idea that the outperformance will last well into 2021 and perhaps beyond.