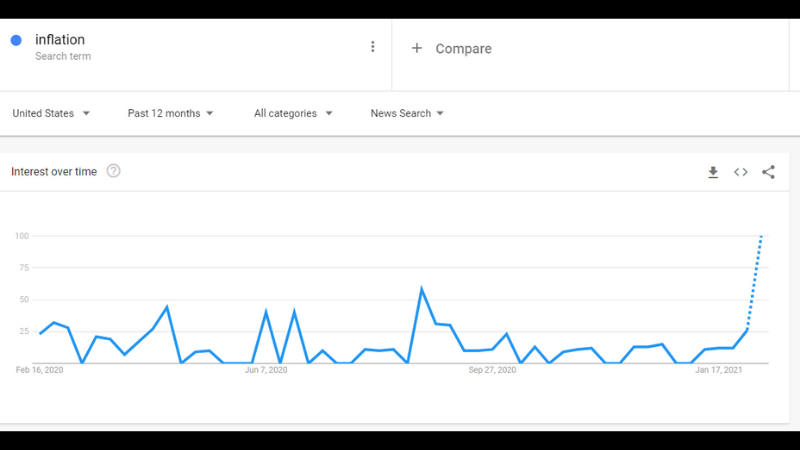

Suddenly inflation worry is everywhere in the financial media although it’s not an actual problem in the real economy. The latest US CPI readings have shown that core price levels remain tame with housing costs actually putting downward pressure on the index – which at 1.4% – is well below the Fed’s 2% target rate.

- Inflation – more a worry than reality

- Small rise rates could wreak havoc with policy

- Inflation more a supply than demand phenomenon

- Post COVID – highly deflationary for services

- Technology offsets policy impulse

Nevertheless, many investors are concerned that inflation expectations will inexorably rise as Fed’s ultra loose monetary policy along with President Biden’s expected 1.9 Trillion stimulus bill will flood the system with liquidity and unleash inflationary pressures.

Cause for Concern

A rise in rates is certainly cause for concern. Higher US rates would not only be damaging to stock valuations which are trading at near record highs precisely because there is no competition from yields, but more importantly would be detrimental to any possibility of further fiscal expansion because US debt service costs would rise exponentially.

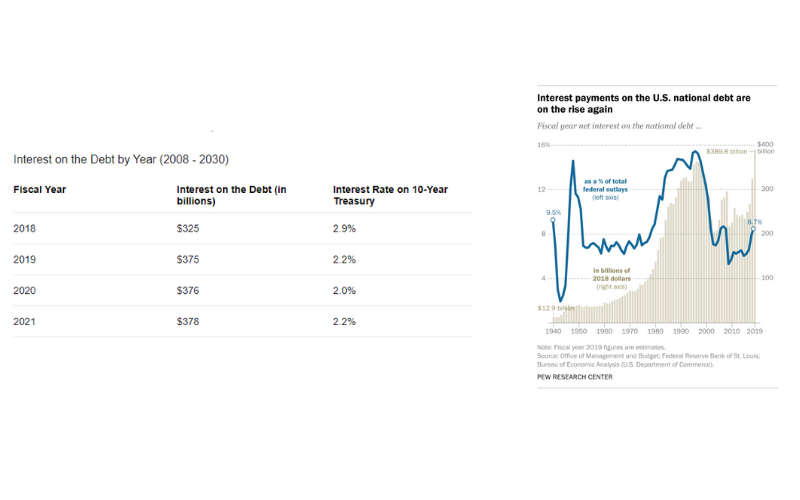

Although US deficits increased by more than 6 Trillion dollars during the Trump Administration the actual cost to the US Treasury was almost imperceptible as decline in rates kept debt service levels steady at about $330 Billion per year. However with US 10 year rates at 1.1% a jump in the long rates by just one percent would in effect double the costs of new US government financing and could quickly double the debt service costs. This sequence of events would put an end to any further fiscal stimulus as the deficit story would suddenly take center stage.

This is the argument of inflationisitas and if it comes true it will no doubt wreak havoc in the financial markets.

Same Fears During GFC Were Totally Wrong

But how realistic is this thesis? Many of the same ideas were put forward in the wake of the Global Financial Crisis and they turned out to be totally false. The massive balance sheet expansion of the Fed had no impact on inflation as prices remained below 2% for most of the decade.

Why?

Inflation – Supply vs. Demand

One possible reason is that inflation is much more of a supply side rather than demand side phenomenon. It can only exist if scarcity of goods persists. At present there are definitely bottlenecks in the system. As Jeff Currie from Goldman Sachs has noted 17 major commodities are currently in deficit with oil the only major exception. If this trend continues then inflationary worries could quickly spiral out of control, A bad weather pattern, a failure of some crops, hoarding by China and the investing landscape would quickly turn cautious. But as COVID recedes and production begins to ramp up to pre-pandemic levels supply chains should begin to replenish and upward pressure on prices should ease.

The commodity story will be the key factor to watch in the first half of 2021, but so far the COVID induced interruptions have not resulted in significant price pressures. In the meantime the China-Amazon complex continues to exert downward pressure on the price of goods as advances in Chinese manufacturing techniques remain a massive deflationary force in the world.

No Pressure from Service Sector

Some analysts have argued that new inflation pressures will arise from the service sector as pent up demand will drive service costs sky high. That is a very dubious thesis. There is no doubt that an initial burst of demand could push prices higher in the travel and hospitality industries, but that will be a one off event. Unlike demand for products, demand for experiences is far more subject to substitution effect so that prices except for the most sought after experiences will not rise much. Furthermore, after so much unused capacity, the industry will be eager to simply find demand and will likely keep prices in check in order to attract as many customers as possible.

But perhaps the most overlooked aspect of the COVID economy is its enormous deflationary impact on the service sector. COVID has shown that so many in-person activities from business meetings to concert recitals to funerals, weddings and family reunions could all be virtualized. Certainly a ZOOM wedding is not nearly as joyful as a destination jaunt to the Caribbean but it is many orders of magnitude less expensive and may become a reality for a certain percentage of the market. This dynamic is sure to repeat itself in a million different ways across thousands of different businesses well after we have all stopped wearing masks in public.

Technology Offsets Policy

While inflationistas wring their hands over every basis point rise in the CRB index and continue to scold both the monetary and fiscal authorities for their profligate ways their argument may be too reliant on economics. Yes Fed’s ultra low interest rate policy regime and Federal governments ultra high budget deficits have laid the foundation for an inflationary impulse. But demand is only one side of the equation. The analysis is missing the very powerful deflationary impact of technology in both goods and services that could completely offset the current policy directives.

For now inflation remains a much bigger worry in the imagination of economists than in the reality of the markets.