In the post Brexit world relations between the UK and the EU are starting to resemble a Cold War rather than a warm peace as two former partners are starting to act like historical enemies that they once were with serious consequences for both economies on either side of the English channel.

The post Brexit climate marked by increased bottlenecks at the border, general friction in trade, and frustrations over the resurgent COVID pandemic is creating a hostile environment for business while threatening to devolve into a race to the bottom for both economies.

On the face of it the UK economy appears to be more vulnerable to post-Brexit woes. It is of course considerably smaller than the European Union which is the third largest economy in the world. The new Brexit rules have created a number of issues at the border as UK businesses must fill out reams of paperwork and a slew of goods must pass EU regulations that were not in place under the prior membership in the union.

The frustration is not only evident amongst the truck drivers and importers at Calais but also amongst a bevy of UK online businesses which now face punitive VAT fees in order to sell into the EU. The one certainty of Brexit is that it has increased the costs of clearance in both goods and services and that is likely to weigh on both price levels and productivity measures of the UK.

Amidst the chaos that has ensued the UK is looking increasingly like an isolated island not only geographically but economically as well. Yet if the UK troubles are well known the EU issues are no better and in some ways possibly worse after the breakup. While the UK is now a small economy with greatly curbed economic and political power, spurned by both the EU and the US, the EU is a lumbering giant that is unable to put one foot in front of the other without tripping over itself.

Nothing has shown the inefficacy of the EU bureaucracy more than the glacial pace of the vaccine roll out as the red tape delays in approval and acquisition issues have set the EU far behind both the US and the UK vaccination counts.

The region is now in danger of succumbing to a bureaucratic morass as both the vaccination plans and the fiscal stimulus disbursements are far too slow for the crisis at hand. Unless EU authorities can ramp up their COVID response plans and reduce new infections the region will almost certainly slip into a double dip recession. That in turn could bring back the highly toxic populist politics of the past which could threaten the very foundations of the region. Already Italy and France show disturbing signs of populist politics and if the current political leaders do not act swiftly the union could face an existential risk of fracture.

Given the pressures on both sides of the Channel, investors need to be highly selective this year. We take a look at the key markets and analyze the best possible ideas for the post-Brexit world.

Indices – Long DAX Short Footsie

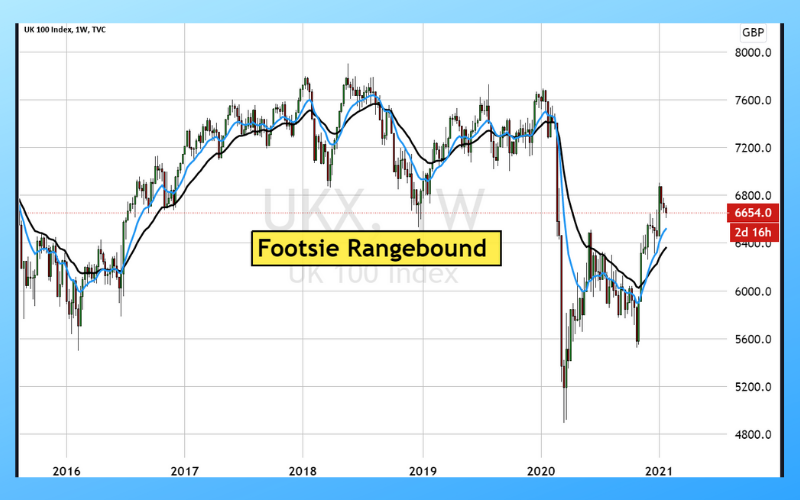

One of the most striking economic themes globally is that manufacturing is performing far better than services in COVID covered world. This is especially true in Europe where there is a massive gap between the Manufacturing and the Services PMI readings. Given the delays in vaccination and the likely hesitancy of consumers to return normal quickly this outperformance of manufacturing is likely to persist for the foreseeable future. This suggests that the Dax which carries a high concentration of industrial giants will outperform the #FTSE100. Indeed looking at the charts the contrast is stark. #DAX is at near all time highs and looks ready to break high on any return to normalcy while the #FTSE100 is range bound showing not upside momentum. So long #DAX vs. #FTSE100 looks to be the trade of 2021.

FOREX – Short EURGBP

The situation is flipped on its head when it comes to the FX markets. For the past year the long #EURGBP trade was one of the easiest one way ideas given the Brexit chaos. However, with the political risk settled the dynamic is likely to reverse. The thesis here is not contingent on UK outperformance (although given the more agile response to the COVID vaccinations, the UK economy may very well outperform on an economic basis. The trade rather is centered on political risk. As we noted earlier the threat of political conflict fracture in the EU over the bureaucratic bungling to the pandemic response could make the market very nervous. Technically the #EURGBP pair has carved out a multi year top at the .9200 level and now has scope to correct towards the .8400 figure as markets move on to post-Brexit themes.

Stocks – High Tech and Biotech

When it comes to individual equities it’s better to focus on global businesses in both the EU and UK that will not be affected by the growing tensions between the two parties. To that end in Europe #ASML looks like a very solid long term play that capitalizes on the growing need for specialized chips for a variety of needs including 5G. Another solid infrastructure company is the Swiss-Swedish conglomerate #ABB which is a leader in industrialized robotics – a trend that will only increase in years ahead.

In the UK the vaccine leader AstraZeneca #AZN will see consistent demand for its product for the foreseeable future as global vaccination campaigns against COVID will likely last for several years at minimum. But the diamond in the rough may be Oxford Biomedica #OXBDF which was heavily involved in the vaccine’s development and manufacture. It will generate more than half of its total revenue from vaccine production and it has £35m by the end of 2021, which is almost half of the total revenue for 2019!. It has many other drugs in the pipeline including therapies for cancer and Parkinson’s.

In the financial sector UK broker IG markets #IGGHY – which dominates the CFD space just announced an acquisition for US options broker Tastytrade. Derivative markets have exploded in the US but are also gaining massive popularity worldwide. As the leader in providing access to multi-asset trading on the retail level IG will be a big beneficiary of this global trend.