- Investors should consider the risk of multiple compression

- Tobacco industry is a case in point

- Risks include rates, marginal growth and exogenous events

With quarterly earnings reports coming up the focus of equity investors will be on guidance for the rest of the year forward. But while growth will be critical to further stock gains investors may be underestimating a far bigger risk to performance – multiple contraction.

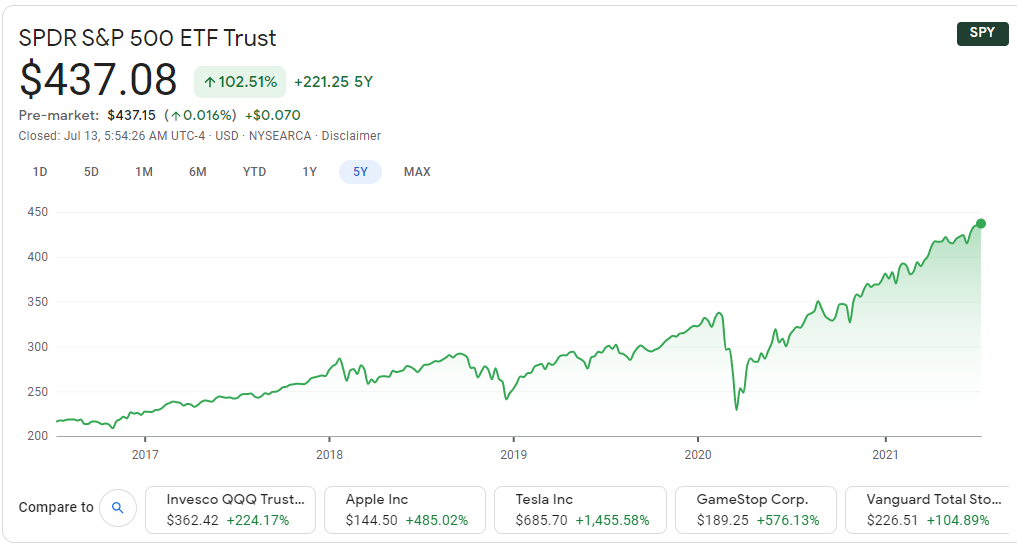

Total return in equities is always a function of two variables – earnings growth and price/earnings multiple. While almost all investors focus on the former, the later may actually be more important. Tobacco stocks are a good case in point. Tobacco stock earrings performance has kept up with the S&P but returns have languished as multiples contracted. As a result Altra returns have been putrid with the stock down 23% in that time while the S&P has more than doubled.

Altria trades as 20 times earnings while the S&P now trades 46.

The compression in earnings multiples could destroy total return regardless of the underlying business performance so let’s consider some of the possible reasons for this outcome.

Rates

Perhaps the single biggest danger to equity market performance is the rise in rates. Little wonder that we’ve seen equity indices at record highs recently given the collapse in 10 year rates. As benchmark 10 year rates have declined from 170 basis points to 135bp stock have soared. That’s because lower yields make every dollar of earnings more and more valuable as the cashflows from bonds decline, investors are willing to pay more for each dollar of earnings. At its most absurd, negative rates if they were perceived to be permanent could send stocks to infinity, but there is no need to engage in thought experiments to see that the single biggest driver of equity gains is the continued decline in yields with the Nasdaq index the prime beneficiary of the “free money” dynamic. That’s why investors would be well advised to keep their eye on rates first, earnings second as the earnings season progresses.

Marginal Earnings Growth

There is little doubt that earnings numbers should improve materially on a year over basis as the economy returns to pre-pandemic activity. But much of the good news is likely priced in. The more important question for investors going forward is how much more organic growth will there be. This is particularly crucial to the mega cap technology companies that dominate index composition. To that end investors should tread with caution as the answers to the question of how much more marginal ad dollars could GOOGL and FB collect, how much more marginal new orders could AMZN fulfill and how many more marginal new subs could NFLX gain over the next twelve months could all disappoint the sky high expectations of the market.

Exogenous Event

With US China and US Russia tensions rising the risks of an exogenous event have increased. Although odds remain relatively low the threat of geo-politocal conflict has escalated and any further deterioration in diplomatic relations could cast a nasty risk off spell on the market. Any de-risking activity no matter how minor always results in multiple compression especially when multiples are elevated as they are now. That’s is why despite equities at record levels investors may want to assume a more defensive posture into the second half of this year.