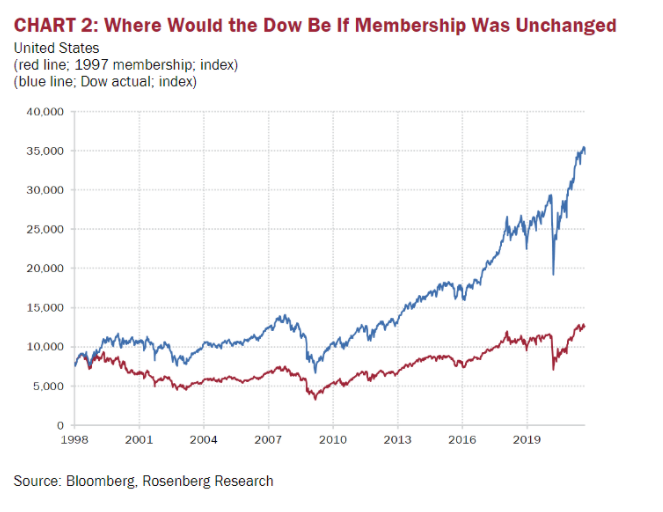

Michael Batnick, head of research at Director of Research at Ritholtz Wealth Management posted a very provocative chart that showed what the performance of the Dow would be if its membership was unchanged from 1998 versus its actual returns for the past two decades. The difference was startling. The dynamic Dow outperformed the static Dow by nearly a factor of four.

This made us wonder if investors would be better served to simply invest their annual allocation into the new Dow entrants rather than the broad index itself. This was an intellectual exercise rather than an academic one. Mainly because we were lazy and busy we simply went back the past two decades rather than all of last century fully cognizant that small sample size and limited lookback window may skew the data. But we took our que from Lord Keynes who famously noted that he would rather be generally right than precisely wrong.

SInce 2009 there were approximately seven additions to the Dow

- In June 2009 Travelers TRV

- In Sept 2012 UnitedHealth UNH

- In Sept 2013 Visa V

- In March 2015 Apple AAPL

- In Sept 2017 DowDupont DD

- In June 2018 Walgreen WBA

- In April 2020 Raytheon RTX

Here is how they performed since they joined the index

- TRV up 400%

- UNH up 800%

- V up 400%

- AAPL up 500%

- DD down 17%

- WBA down 13%

- RTX up 40%

An investor who put $10,000 into each new addition to the Dow over the past decade would have seen $70,000 turn into $237,000. That’s pretty good, but an investor who simply put $70,000 into the index in June 2009 would now have $315,000 or $78,000 more proving once again that time is still the most important variable in investing. But that is not really a fair comparison – not the least because putting all of your capital in the market in June 2009 was essentially timing the generational bottom. To do a fair comparison we need to assume that our investor would allocate to the index on the exact same schedule as the additions to the Dow. Given those parameters the index investor would see his $70,000 turn to only $144,000 or a whopping $93,000 less than the investor who only bought the new additions to the index.

So is there anything to be learned from this exercise? As I noted, it’s limited and likely very skewed by bull market data. These Dow additions have been extraordinary picks and there is absolutely no guarantee that future additions will be nearly as valuable. The last three picks simply confirm the idea that this strategy can be a dud as well. Still, there is something to be said for conventional wisdom (which in its kinder form can be described as the wisdom of the crowds). If we learned anything over the past few decades its that conventional wisdom in the form of the index fund can be far better than our own. Although companies that are added to the Dow are often well past their most meteoric growth stage, it does not mean that they may not enjoy many years of market-beating growth. So perhaps a Solomonic compromise is in order. Investors should continue to allocate a fixed amount of their savings to the index fund on an annual basis to create long term wealth via equity returns, but they may consider making an additional contribution to the newly added name effectively “overweighting” the index with the new members. This a modest pyramiding scheme into the bluest of the blue chips and it may provide outsized returns in years ahead.